08:00 AM – 06:00 PM

08:00 AM – 03:00 PM

Closed

The property owners usually learn about a four-point assessment when an insurance carrier requests additional documentation before issuing or renewing coverage. The pricing is an important consideration but it’s also crucial to understand the purpose behind this evaluation. A four-point review examines the condition of key components that significantly influence a building's risk profile. The findings help insurance providers determine eligibility and assess potential exposure to future claims. The Four Point Inspection Cost Orlando FL can vary based on factors i.e. building age, square footage, accessibility, and reporting requirements. The older structures require closer examination because aging materials and outdated systems may present concerns. At A-1 Home Inspection Services, the goal is to provide clear, factual observations that help clients make informed decisions. The inspectors examine in detail and help you know why these reports matter, so you can continue the process with greater confidence and fewer surprises.

(407) 721-5329

a1homeinspectfl@gmail.com

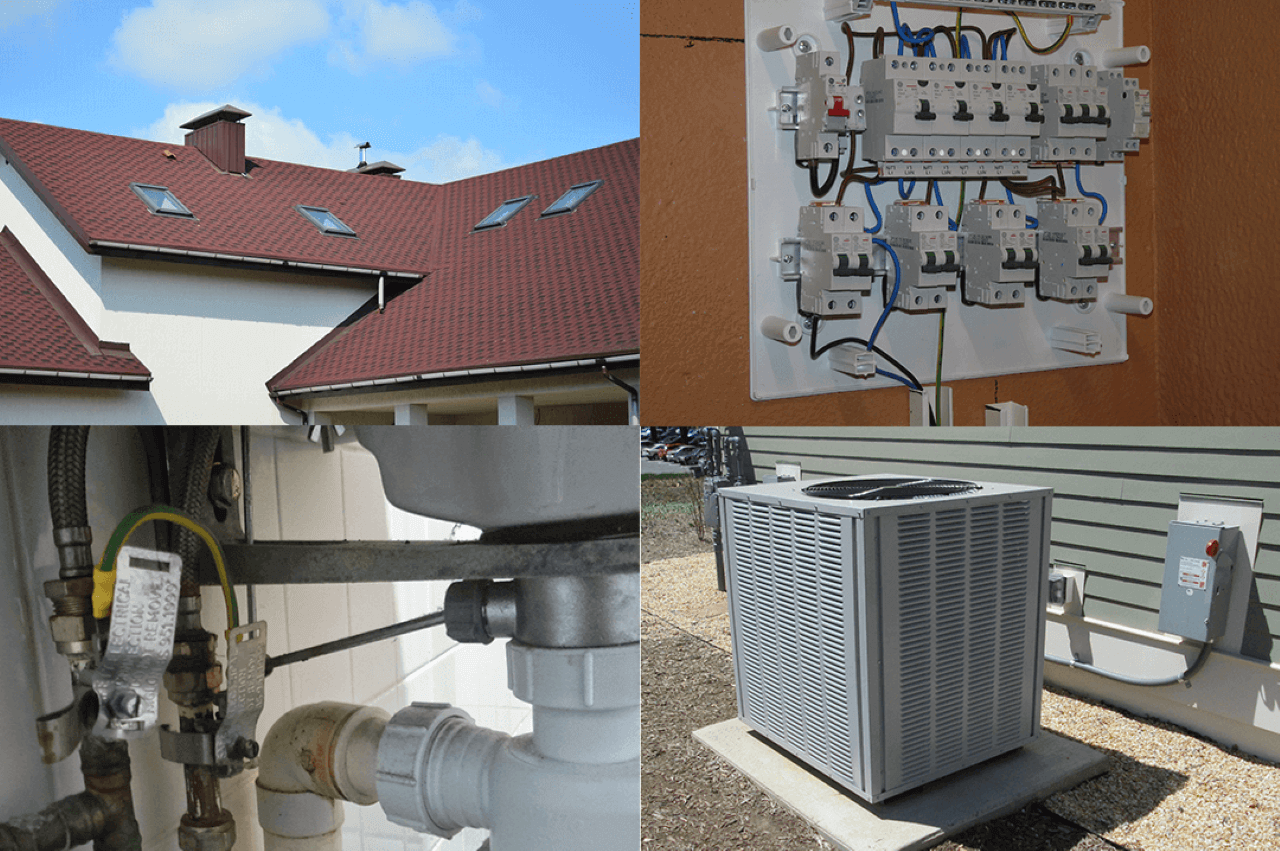

A four-point assessment concentrates on four major areas of a structure: the roofing system, electrical components, plumbing network, and heating and cooling equipment. These elements are reviewed because they play a major role in overall safety, functionality, and insurability.

Insurance companies frequently request this type of evaluation for older buildings to gain a clearer understanding of their current condition. The report focuses specifically on these critical categories. The resulting documentation offers insurers relevant information about age, condition, and observable concerns that could affect future coverage decisions.

A standard residential assessment examines many accessible components throughout a dwelling, including structural elements, interiors, exteriors, and appliances. A four-point home evaluation has a narrower scope and concentrates only on the roofing assembly, electrical distribution, plumbing components, and climate-control equipment.

The homeowners need this report when purchasing an older residence, renewing an insurance policy, changing carriers, or satisfying underwriting requirements. Because the review targets specific categories, it provides focused information that helps insurers evaluate potential risks.

The roofing portion of the assessment documents visible conditions that affect weather resistance and long-term performance. Inspectors note the estimated age of materials, signs of deterioration, damaged coverings, previous repairs, and any observable concerns that could allow moisture intrusion. Photographs are commonly included to support the findings.

This stage involves examining readily accessible electrical components to identify potential safety concerns and determine the general condition. The review covers service panels, wiring methods, breakers, grounding, and other visible equipment. Inspectors document outdated configurations, evidence of overheating, or installations that may warrant further evaluation.

The inspectors observe visible supply lines, drainage components, fixtures, and water-heating equipment. The goal is to locate leaks, corrosion, material types, and other conditions that could contribute to water-related damage. The team at A-1 Home Inspection Services gives particular attention to aging piping systems that have a history of failures.

The heating and cooling portion focuses on the age, apparent condition, and operation of climate-control equipment. The inspectors document observable issues involving major components, including air handlers, condensers, and related equipment, when accessible. The professional notes signs of excessive wear, damage, or deferred maintenance within the report. This information helps insurers assess the chances of equipment problems and provide property owners with useful insight.

No two buildings are exactly alike, which is why inspection fees often differ. A newer residence with easily accessible systems needs less time than an older structure that contains aging materials or complex layouts. The multi-unit facilities, larger floor plans, and properties with limited access points can also increase the level of work involved. In some situations, additional photographs, insurer-specific forms, or supplemental documentation can be requested. These variables contribute to differences in pricing from one location to another.

The homeowners encounter this requirement during an insurance application, policy renewal, or carrier change. The older houses are frequently subject to additional review because insurers want updated information regarding major building systems.

A four-point assessment is also useful before listing a residence for sale or planning significant upgrades. Receiving an objective overview of key components allows owners to address concerns proactively and better understand the current condition of important parts of the dwelling.

The commercial buildings have larger and more complex systems than single-family residences. The roofing assemblies cover extensive areas, mechanical equipment can serve multiple occupants, and utility infrastructure is frequently designed for higher usage demands. Due to these differences, insurers commonly seek detailed information about the state of critical components.

A focused evaluation helps document observable conditions, identify aging equipment, and provide valuable information for risk assessment, property management, and insurance decisions.

Local experience can make a significant difference in a four-point evaluation. Inspectors familiar with Orlando properties understand common construction methods, regional weather impacts, and insurance expectations associated with Florida buildings. This knowledge helps identify conditions frequently seen in the area and ensures reports contain relevant information insurers may request. Property owners searching for Four Point Inspection Near Me are often looking for professionals who understand local housing trends, environmental factors, and industry requirements that influence coverage decisions.

Verify that the inspection team meets state requirements and follows recognized industry standards.

Look for reports that include photographs, observations, and easy-to-understand explanations.

Companies familiar with underwriting requirements can provide documentation that aligns with insurer expectations.

Choose a provider that answers questions promptly and straightforwardly explains findings.

At A-1 Home Inspection Services, clients benefit from experienced inspectors, comprehensive reporting, industry knowledge, and a commitment to delivering objective information that supports informed property decisions. Get in touch today!

A four-point inspection provides information about a property's roof, electrical system, plumbing, and HVAC equipment. Insurance companies use the report to evaluate potential risks and determine eligibility for coverage, particularly for older buildings.

The timeframe depends on the property's size and accessibility. Most residential evaluations can be completed relatively quickly, while larger or more complex structures require additional time for documentation and observation.